Does Valuation Still Matter When Everyone is Overpaying?

(I had this one saved for paid subscribers, but honestly, I think this topic is too important to keep behind a paywall. Free for everyone for a limited time. Enjoy!)

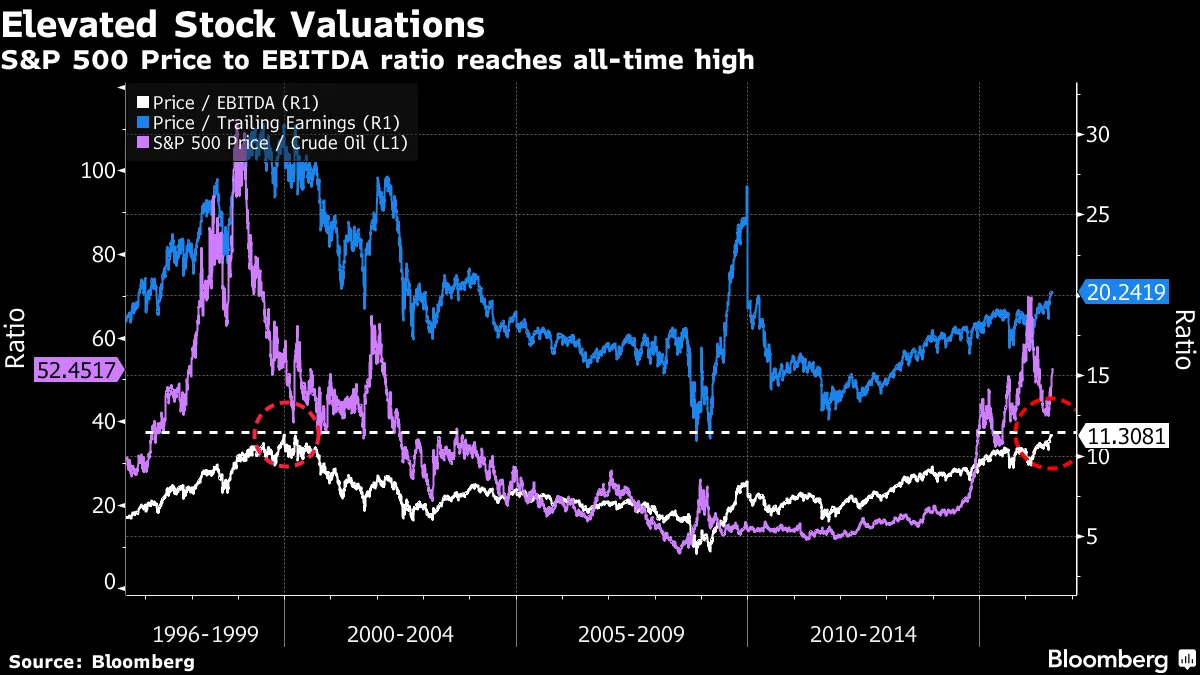

I recently watched an interesting Goldman Sachs interview with David Craver from Lone Pine Capital. He observed that the market has changed in a pretty fundamental way, where high valuations among industry giants are now the norm, and stock volatility remains at historical highs.

Craver noted that early in his career, a company with a market capitalization exceeding $200 billion and a P/E ratio above 20x was seen as a 'disaster waiting to happen.' Yet, here in 2026, dozens of such companies dominate the market, with their valuations continuing to climb. It’s an incredibly insightful interview, and it must worth your time if you follow markets :D

This interview raises a question that every investor must have thought about: In an era dominated by passive index funds and algorithmic trading, have traditional valuation principles become relics of the past? I have some own perspective on this market structure shift and would love to share a bit of my view. I look forward to hearing your thoughts also hence please feel free to leave comment and let me know about your thoughts.

My answer is no, but it's complicated. Valuation has not become outdated, but the market's pricing mechanism has been structurally changed in ways that create dangerous illusions. As rational investors, we must recognize that valuation should remain the primary anchor in distinguishing investment from speculation, even if the gap between current valuations and eventual reality has become wider and more volatile than in previous eras. (I think that investment and speculation are not mutually exclusive; they can and do co-exist, a point I will elaborate on later.)

If you have studied on modern equity market structure, you will recognize how passive investing introduces a structural bias toward overvaluation. In this environment, the largest firms command the highest premiums, and volatility often rises alongside the surge in index inflows. This shift is a fundamental change in the way capital moves through the market.

Traditionally, investing was a human process of deliberate decision-making based on business fundamentals, moats, and intrinsic value. Simply you read the business, decided it was cheap, and bought it. When a stock became overextended relative to its earnings power, rational investors would reallocate capital elsewhere. This acted as a natural ceiling on valuations, or we called it as a built-in self-correcting mechanism.

Passive investing breaks this mechanism. When you invest in an S&P 500 index fund, you're not making 500 individual investment decisions. You're making one decision: to own the market. Capital is then algorithmically allocated based on market-cap weights, triggering a self-reinforcing feedback loop: the largest firms attract the most significant inflows, driving their prices higher. This, in turn, increases their index weighting, which attracts even more capital.

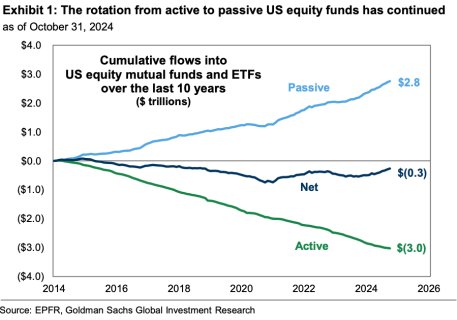

This cycle persists until discretionary or rational investors decide valuations have become so disconnected from reality that they must reallocate their portfolios. However, the 'tipping point' is harder to reach than ever. As of late 2025, passive assets in ETFs and mutual funds reached approximately $19 trillion, overshadowing the $16 trillion held in active funds, a staggering leap from a mere 15% passive share in 2000. Furthermore, over 70% of daily equity trading volume is now driven by passive flows, arbitrage, and quantitative strategies. Consequently, the market must wait until both human insight and algorithmic models agree that prices are too high for inflows to finally subside.

The mechanics become even more concerning when examining overvalued stocks. If a large-cap firm is already overextended, passive flows exacerbate that overvaluation. These overpriced stocks then become increasingly risky for active investors, who find it difficult to offset the sheer momentum of passive flows, further distancing price from intrinsic value.

If you do not understand what does it mean, here’s the cycle:

A stock becomes overvalued through initial enthusiasm or genuine business success

Its market cap grows, increasing its weight in major indexes

Passive funds automatically buy more of this now-expensive stock

Active investors who recognize the overvaluation become reluctant to short/sell it because passive flows keep pushing the price higher

With fewer active investors willing to bet against it, the stock price must rise even further to compensate the remaining skeptics for their risk

This higher price increases the index weight further, and the cycle repeats, until the valuation is too high that algorithmic models agree that prices are too high.

Layered on top of passive flows is the growing dominance of quantitative and algorithmic trading strategies. These systems operate on a fundamentally different logic than traditional fundamental analysis.

Quantitative strategies seek factors like momentum, volatility, and statistical correlations: not business fundamentals. When these algorithms detect an upward trend, they buy; when volatility shifts, they adjust positions based on pre-programmed triggers.

We can see stock volatility around events is now at historically high levels and often detached from qualitative fundamental news. A company can report strong earnings, but if the algorithmic signals say “sell” based on technical factors, the stock may plummet despite positive fundamentals. Conversely, a company with deteriorating fundamentals may see its stock soar if momentum algorithms detect an uptrend.

This creates lots of “pricing noise”: short-term price movements that have little to do with the underlying business reality. You may also always hear the explanation of surprise price action as “Market has priced in”.

For fundamental investors, these noise are both frustrating and potentially opportunistic. I believe this situation actually works in favor of value investors, but it requires stronger belief in your own analysis. To succeed, you need the mental strength to trust your own logic and stick to your strategy, no matter how much noise there is in the market.

That said, I am not a 'permabear' who dismisses the market as simply irrational.. It’s important to acknowledge that some of the elevated valuations we observe today reflect genuine economic transformations, not just financial engineering. The digital and AI-driven economy exhibits characteristics that traditional industrial firms never possessed:

High Marginal Profitability: Once software is developed, scaling costs are negligible. A giant like Microsoft can add millions of subscribers with minimal incremental expense.

Network Effects: Platforms like Facebook become exponentially more valuable as more users join, creating natural monopolies.

Winner-Take-All Dynamics: In digital markets, the leader often captures the lion’s share of value, leaving the runner-up with a mere fraction.

Rapid scalability: A successful digital product can reach global scale in years rather than decades.

These characteristics do justify higher valuations than we would assign to, say, a steel manufacturer or a retail chain. However, the real question isn't whether these businesses deserve a premium, but whether the current premiums are sustainable.

If AI truly delivers a massive productivity leap, allowing firms to generate significantly higher output with fewer inputs, and we remain in a favorable macro environment with mild inflation and a flexible Federal Reserve, then risk assets still have fertile ground. In such a scenario, high P/E ratios might actually be justified. But the operative word here is ‘if’.

History teaches us to remain cautious regarding technological hype cycles. While the internet genuinely transformed the global economy, its long-term impact did not prevent the catastrophic mispricing of the year 2000. The titans that eventually came to dominate, such as Amazon and Google, were active during the bubble, yet they still saw their valuations decimated when short-term reality failed to match inflated expectations.

I must reiterate: I am not claiming that AI itself is a bubble. However, AI can, and likely will, produce 'bubble companies.' We must be cautious in identifying and excluding these firms from our portfolios, even if their potential appears compelling in a PowerPoint presentation deck. Success on paper is no substitute for a sustainable business model.

In the interview, Craver pointed out that because most market participants, both passive and quantitative, have largely abandoned deep fundamental valuation, but a unique window of opportunity has opened. For fundamental investors, the challenge is to identify which high valuations are justified by durable business quality and which are merely artifacts of capital flows. To outperform the market in this era, we need to learn how to discriminate rather than simply reject all high-valuation stocks as bubbles. We must distinguish between:

Companies with genuinely exceptional economics that justify premium pricing

Companies whose valuations reflect nothing more than their index weight or a speculative narrative, fueled by passive inflows.

Companies whose valuations embed expectations that may be theoretically possible, but are statistically improbable.

Mastering this distinction is what separates a disciplined investor from the rest of the herd.

Modern valuation discussions often invoke the concept of duration, the idea that exceptional businesses deserve high multiples because their competitive advantages will persist for decades. This argument has merit but contains a fatal flaw: it dramatically increases your exposure to changes in the discount rate (interest rates and risk premiums) and to execution risk over very long time horizons.

When you pay 40x p/e for a stock, you’re implicitly betting that:

The business will maintain its competitive advantage for decades

Management will continue making good decisions for decades

No disruptive technology or business model will emerge

Regulatory environments won’t turn hostile

The broader economy won’t enter a prolonged downturn

Interest rates won’t rise significantly

The most important is betting: Market are willing to pay same valuation at this level throughout the time. That’s a lot of things that need to go right. And if even one goes wrong, the duration premium collapses rapidly.

Concept of margin of safety was not a suggestion for conservative investors, it was a fundamental principle of rational investing. The margin of safety is the difference between what you pay and what something is worth, and it exists to protect you from the inevitable errors in your analysis and the unpredictable turns of fate.

When you pay full price or a premium for an asset, you’re assuming your analysis is perfect and the future will unfold as expected. This is a form of hubris that markets have always punished eventually.

The modern market structure has conditioned many investors to believe that paying premium prices is normal and safe because this time is different with digital economics, network effects, and AI. But every previous generation of investors believed their era was fundamentally different too. The specifics change; the psychology doesn’t.

The greatest danger of extended bull markets supported by passive flows is not the overvaluation itself. It’s the psychological unpreparedness for the inevitable reversal.

Bear markets follow a familiar script: denial, then panic, then the moment when even the true believers finally give up.

The same passive flows that pushed prices higher work in reverse. Index funds experiencing redemptions must sell their largest holdings, the very stocks that got most overvalued during the bull market. While passive funds aren’t necessarily forced to sell during normal market fluctuations, mass investor redemptions during bear market or similar event could trigger a downward spiral.

The mental pressure is heavy: fear leads to a bad cycle where falling prices cause panic selling. This drops prices even further, making people feel crushed and making their earlier hope look foolish

During bull markets, investors justify high p/e ratios by pointing to growth prospects, competitive advantages, and “new era”. These narratives have power because they’re partially true and because rising prices seem to validate them.

In bear markets, sentiment reverses completely. As earnings expectations fall, investors reassess valuations, leading to sustained selling pressure. But it’s not just earnings that fall, the multiple investors are willing to pay for those earnings collapses.

A stock trading at 40 times earnings might see earnings fall 20%, but the P/E multiple might compress from 40 to 15. That’s not a 20% decline. It’s a 70% decline.

Original price: $100 (Earnings of $2.50 × P/E of 40)

New earnings: $2.00 (down 20%)

New multiple: 15 (reflecting pessimism)

New price: $30 (down 70%)

Meanwhile, a stock that entered the bear market at 12 times earnings might see the same 20% earnings decline but only compress to a P/E of 10:

Original price: $100 (Earnings of $8.33 × P/E of 12)

New earnings: $6.67 (down 20%)

New multiple: 10

New price: $66.70 (down 33%)

The high-valuation stock lost more than twice as much, even though the underlying business deterioration was identical. This is the brutal arithmetic of multiple contraction.

Many investors convince themselves that owning quality companies protects them from valuation risk. This is dangerously wrong.

Quality companies deserve premium valuations, but there’s a vast difference between a deserved premium and an excessive one. Microsoft is genuinely one of the highest-quality businesses ever created, but that didn’t prevent its stock from losing more than 60% of its value from 2000 to 2002, and taking 15 years to meaningfully exceed its 2000 peak. The business quality was real; the valuation was still wrong.

Research on bear markets shows that while high starting valuations don’t predict when bear markets will begin, they are strongly correlated with the severity of the decline when it eventually arrives. Your protection is not the quality of the business; it’s the price you paid relative to that quality.

The goal of this article is not to convince you to avoid all stocks with elevated valuations, that might cause you to miss genuine opportunities. Instead, the goal is to construct a portfolio that can survive and even benefit from the eventual return to more normal valuation standards.

Perhaps the hardest part of maintaining valuation discipline today is the psychological pressure. When stocks you consider overvalued continue to climb for years while you hold cash or own modest businesses that lag behind, the temptation to abandon your principles becomes intense.

It comes down to one question: Are you an investor or a speculator?

Investors buy businesses at prices that offer reasonable prospects for satisfactory returns based on likely business performance. They’re content with good returns over time and accept that they’ll sometimes miss euphoric runs.

Speculators buy assets hoping to sell them to someone else at higher prices, with returns dependent on continuing enthusiasm from other market participants rather than underlying business performance.

Neither approach is ‘better,’ but they require different mindset. Speculating during a bubble can be profitable if you have perfect timing, but most people don’t, which is why most speculators eventually lose their gains.

If you’re going to be an investor, and that’s what this article assumes, then valuation discipline is non-negotiable. You will sometimes look foolish. You will miss some gains. But you will survive the inevitable periods when prices reconnect with reality.

At the end, the key to outperforming today’s market is learning how to navigate both worlds: integrating the discipline of an investor with an understanding of human and algorithmic behavior.

No matter you are an investor or a speculator, you need to:

Acknowledge that market structures have fundamentally changed. Passive flows and quantitative trading have changed short and medium-term pricing dynamics in ways that can persist for years. Fighting these trends blindly is expensive and frustrating.

Maintain that valuation remains the primary anchor distinguishing investment from speculation. No structural change in market mechanics can rewrite basic mathematics: your returns equal business performance plus or minus the change in the valuation multiple you paid.

The real challenge is holding two conflicting thoughts simultaneously:

“This stock may continue rising despite excessive valuation because of technical factors.”

“I will not own it at current prices because eventual mean reversion is certain, even if timing is uncertain.”

This isn’t about market timing. It is a refusal to participate in unsustainable dynamics, even while acknowledging they may last longer than seems rational.

Valuation discipline is your high ground. The passive flows and algorithmic momentum will eventually reverse. When they do, the old rules namely multiple contraction, flight to safety, desperate searches for cash flow and dividends over distant growth promises, will return with force.

Maintain your discipline. Wait for your opportunities. Remember that in investing, it’s not what you make when everything goes right that determines success. It’s what you avoid when everything goes wrong.

The old valuation rules haven’t been broken. They’ve been temporarily suspended by unusual market dynamics. But suspended is not eliminated. And when they return, as they always do, you want to be among those who never forgot they existed.

Criminally underrated account: keep it up!

Great reminder that the market is driven by its own ruthless logic, not by optimistic narratives.

I also recently read a paper on index investing. The authors showed that there are economic mechanisms that actually decrease correlation between assets inside the index. This effect is offset by capital inflows, so it is invisible. But suppose the regime changes, retail loses trust in the stock market, and inflows drop. In that case, stocks can become super-sensitive to fundamentals, and valuation will matter more than ever.